Pure Price Action Breakout with 1:5 RR

Description of the Price Action Trading Script (Pine Script v6)

Overview

This script is a pure price action-based breakout strategy designed for TradingView. It identifies key breakout levels and executes long and short trades based on market structure. The strategy ensures a minimum risk-to-reward ratio (RR) of 1:5, aiming for high profitability with well-defined stop-loss and take-profit levels.

How the Script Works

1️⃣ Breakout Identification

The script uses a lookback period to find the highest high and lowest low over the last n bars.

A bullish breakout occurs when the price closes above the previous highest high.

A bearish breakout happens when the price closes below the previous lowest low.

2️⃣ Entry & Exit Strategy

Long Entry: If a bullish breakout is detected, the script enters a long position.

Short Entry: If a bearish breakout is detected, the script enters a short position.

The stop-loss is placed at the recent swing low (for long trades) or recent swing high (for short trades).

The target price is calculated based on a risk-to-reward ratio of 1:5, ensuring profitable trades.

3️⃣ Risk Management

The stop-loss prevents excessive losses by exiting trades when the market moves unfavorably.

The strategy ensures that each trade has a reward potential at least 5 times the risk.

Positions are executed based on price action only, without indicators like moving averages or RSI.

4️⃣ Visual Representation

The script plots breakout levels to help traders visualize potential trade setups.

Entry points, stop-loss, and take-profit levels are labeled on the chart for easy tracking.

Key Features & Benefits

✔ Pure Price Action – No lagging indicators, only real-time price movements.

✔ High Risk-to-Reward Ratio (1:5) – Ensures high-profit potential trades.

✔ Real-time Entry & Exit Signals – Provides accurate trade setups.

✔ Dynamic Stop-loss Calculation – Adjusts based on recent market structure.

✔ Customizable Parameters – Lookback periods and risk ratios can be modified.

Cerca negli script per "stop loss"

EMA SHIFT & PARALLEL [n_dot]BINANCE:ETHUSDT.P

This strategy was developed for CRYPTO FUTURES, (the settings for ETHUSDT.P) . I aimed for the strategy to function in a live environment, so I focused on making its operation realistic:

When determining the position, only 80% (adjustable) of the available cash is invested to reduce the risk of position liquidation.

I account for a 0.05% commission, typical on the futures market, for each entry and exit.

Concept:

I modified a simple, well-known method: the crossover of two exponential moving averages (FAST, SLOW) generates the entry and exit signals.

I enhanced the base idea as follows:

For the fast EMA, I incorporated a multiplier (offset) to filter out market noise and focus only on strong signals.

I use different EMAs for long and short entry points; both have their own FAST and SLOW EMAs and their own offset. For longs, the FAST EMA is adjusted downward (<1), while for shorts, it is adjusted upward (>1). Consequently, the signal is generated when the modified FAST EMA crosses the SLOW EMA.

Risk Management:

The position includes the following components:

Separate stop-losses for long and short positions.

Separate trailers for long and short positions.

The strategy operates so that the entry point is determined by the EMA crossover, while the exit is governed only by the Stop Loss or Trailer. Optionally, it can be set to close the position at the EMA recrossing ("Close at Signal").

Trailer Operation:

An entry percentage and offset are defined. The trailer activates when the price surpasses the entry price, calculated automatically by the system.

The trailer closes the position when the price drops by the offset percentage from the highest reached price.

Example for trailer:

Purchase Price = 100

Trailer Enter = 5% → Activation Price = 105 (triggers trailer if market price crosses it).

Trailer Offset = 2%

If the price rises to 110, the exit price becomes 107.8.

If the price goes to 120, the exit price becomes 117.6.

If the price falls below 117.6, the trailer closes the position.

Settings:

Source: Determines the market price reference.

End Close: Closes positions at the end of the simulation to avoid "shadow positions" and provide an objective result.

Lot proportional to free cash (%): Only a portion of free cash is invested to meet margin requirements.

Plot Short, Plot Long: Simplifies displayed information by toggling indicator lines on/off.

Long Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast down shift: Adjustment factor for FAST EMA.

Stop Loss long (%): Percent drop to close the position.

Trailer enter (%): Percent above the purchase price to activate the trailer.

Trailer offset (%): Percent drop to close the position.

Short Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast up shift: Adjustment factor for FAST EMA.

Stop Loss short (%): Percent rise to close the position.

Trailer enter (%): Percent below the purchase price to activate the trailer.

Trailer offset (%): Percent rise to close the position.

Operational Framework:

If in a long position and a short EMA crossover occurs, the strategy closes the long and opens a short (flip).

If in a short position and a long EMA crossover occurs, the strategy closes the short and opens a long (flip).

A position can close in three ways:

Stop Loss

Trailer

Signal Recrossing

If none are active, the position remains open until the end of the simulation.

Observations:

Shifts significantly deviating from 1 increase overfitting risk. Recommended ranges: 0.96–0.99 (long) and 1.01–1.05 (short).

The strategy's advantage lies in risk management, crucial in leveraged futures markets. It operates with relatively low DrawDown.

Recommendations:

Bullish Market: Higher entry threshold (e.g., 6%) and larger offset (e.g., 3%).

Volatile/Sideways Market: Tighter parameters (e.g., 3%, 1%).

The method is stable, and minor parameter adjustments do not significantly impact results, helping assess overfitting: if small changes lead to drastic differences, the strategy is over-optimized.

EMA Settings: Adjust FAST and SLOW EMAs based on the asset's volatility and cyclicality.

On the crypto market, especially in the Futures market, short time periods (1–15 minutes) often show significant noise, making patterns/repetitions hard to identify. I recommend setting the interval to at least 1 hour.

I hope this contributes to your success!

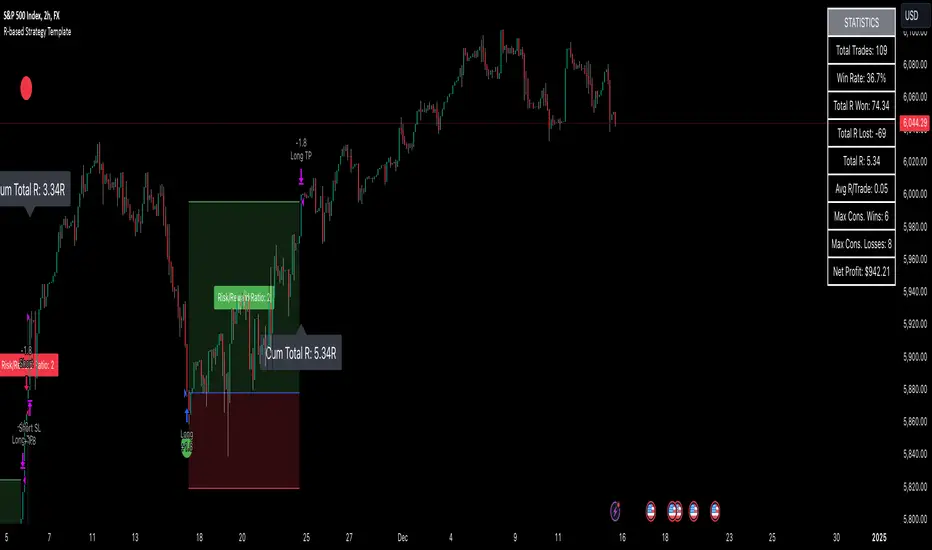

R-based Strategy Template [Daveatt]Have you ever wondered how to properly track your trading performance based on risk rather than just profits?

This template solves that problem by implementing R-multiple tracking directly in TradingView's strategy tester.

This script is a tool that you must update with your own trading entry logic.

Quick notes

Before we dive in, I want to be clear: this is a template focused on R-multiple calculation and visualization.

I'm using a basic RSI strategy with dummy values just to demonstrate how the R tracking works. The actual trading signals aren't important here - you should replace them with your own strategy logic.

R multiple logic

Let's talk about what R-multiple means in practice.

Think of R as your initial risk per trade.

For instance, if you have a $10,000 account and you're risking 1% per trade, your 1R would be $100.

A trade that makes twice your risk would be +2R ($200), while hitting your stop loss would be -1R (-$100).

This way of measuring makes it much easier to evaluate your strategy's performance regardless of account size.

Whenever the SL is hit, we lose -1R

Proof showing the strategy tester whenever the SL is hit: i.imgur.com

The magic happens in how we calculate position sizes.

The script automatically determines the right position size to risk exactly your specified percentage on each trade.

This is done through a simple but powerful calculation:

risk_amount = (strategy.equity * (risk_per_trade_percent / 100))

sl_distance = math.abs(entry_price - sl_price)

position_size = risk_amount / (sl_distance * syminfo.pointvalue)

Limitations with lower timeframe gaps

This ensures that if your stop loss gets hit, you'll lose exactly the amount you intended to risk. No more, no less.

Well, could be more or less actually ... let's assume you're trading futures on a 15-minute chart but in the 1-minute chart there is a gap ... then your 15 minute SL won't get filled and you'll likely to not lose exactly -1R

This is annoying but it can't be fixed - and that's how trading works anyway.

Features

The template gives you flexibility in how you set your stop losses. You can use fixed points, ATR-based stops, percentage-based stops, or even tick-based stops.

Regardless of which method you choose, the position sizing will automatically adjust to maintain your desired risk per trade.

To help you track performance, I've added a comprehensive statistics table in the top right corner of your chart.

It shows you everything you need to know about your strategy's performance in terms of R-multiples: how many R you've won or lost, your win rate, average R per trade, and even your longest winning and losing streaks.

Happy trading!

And remember, measuring your performance in R-multiples is one of the most classical ways to evaluate and improve your trading strategies.

Daveatt

IU EMA Channel StrategyIU EMA Channel Strategy

Overview:

The IU EMA Channel Strategy is a simple yet effective trend-following strategy that uses two Exponential Moving Averages (EMAs) based on the high and low prices. It provides clear entry and exit signals by identifying price crossovers relative to the EMAs while incorporating a built-in Risk-to-Reward Ratio (RTR) for effective risk management.

Inputs ( Settings ):

- RTR (Risk-to-Reward Ratio): Define the ratio for risk-to-reward (default = 2).

- EMA Length: Adjust the length of the EMA channels (default = 100).

How the Strategy Works

1. EMA Channels:

- High-based EMA: EMA calculated on the high price.

- Low-based EMA: EMA calculated on the low price.

The area between these two EMAs creates a "channel" that visually highlights potential support and resistance zones.

2. Entry Rules:

- Long Entry: When the price closes above the high-based EMA (crossover).

- Short Entry: When the price closes below the low-based EMA (crossunder).

These entries ensure trades are taken in the direction of momentum.

3. Stop Loss (SL) and Take Profit (TP):

- Stop Loss:

- For long positions, the SL is set at the previous bar's low.

- For short positions, the SL is set at the previous bar's high.

- Take Profit:

- TP is automatically calculated using the Risk-to-Reward Ratio (RTR) you define.

- Example: If RTR = 2, the TP will be 2x the risk distance.

4. Exit Rules:

- Positions are closed at either the stop loss or the take profit level.

- The strategy manages exits automatically to enforce disciplined risk management.

Visual Features

1. EMA Channels:

- The high and low EMAs are dynamically color-coded:

- Green: Price is above the EMA (bullish condition).

- Red: Price is below the EMA (bearish condition).

- The area between the EMAs is shaded for better visual clarity.

2. Stop Loss and Take Profit Zones:

- SL and TP levels are plotted for both long and short positions.

- Zones are filled with:

- Red: Stop Loss area.

- Green: Take Profit area.

Be sure to manage your risk and position size properly.

MicuRobert EMA Cross StrategyThis is a repost of a old strategy that cant be updated anymore, it was a request for a user made in Oct, 6, 2015

Here's a possible engaging description for the tradingview script:

**MicuRobert EMA Cross V2: A Powerful Trading Strategy**

Join the ranks of successful traders with this advanced strategy, designed to help you profit from market trends. The MicuRobert EMA Cross V2 combines two essential indicators - Exponential Moving Average (EMA) and Divergence EMA (DEMA) - to generate buy and sell signals.

**Key Features:**

* **Trading Session Filter**: Only trade during your preferred session, ensuring you're in sync with market conditions.

* **Trailing Stop**: Automatically adjust stop-loss levels to lock in profits or limit losses.

* **Customizable Trade Size**: Set the size of each trade based on your risk tolerance and trading goals.

**How it Works:**

The script uses two EMAs (5-period and 34-period) to identify trends. When the shorter EMA crosses above the longer one, a buy signal is generated. Conversely, when the shorter EMA falls below the longer one, a sell signal is triggered. The strategy also incorporates divergence analysis between price action and the EMAs.

**Visual Aids:**

* **EMA Plots**: Visualize the two EMAs on your chart to gauge market momentum.

* **Buy/Sell Signals**: See when buy or sell signals are generated, along with their corresponding entry prices.

* **Trailing Stop Lines**: Monitor stop-loss levels as they adjust based on price action.

**Get Started:**

Download this script and start trading like a pro! With its robust features and customizable settings, the MicuRobert EMA Cross V2 is an excellent addition to any trader's arsenal.

~Llama3

Z The Good Stuff +I created this script to have a couple datapoints that I want to look at when going through charts to find trade ideas. Qullamaggie is one of my biggest inspirations and I built in a couple of his concepts with a touch to help me with sizing properly, all explained below:

Box 1: ADR %, Average Daily Range, gives and indication of how volatile the stock is. It uses the 20 day average % move of the current stock on the chart.

Box 2: LOD Distance, low of day distance is a quality of life element I created. It calculates the low for the current candle and color codes it red or green depending on if it's higher or lower than the daily ADR. The logic is that if a stock has an average speed, buying on a setup it is preferred if the stop distance (assuming a low of day stop) should be less than the ADR to improve the odds of more upside.

Box 3: Todays DV, this shows a rough estimate of how much money was traded on the particular day.

Box 4: ADV 20 days, similar to above this shows the 20 day $ traded average. The point to look at it is to have a better idea what position size is possible to not get stuck in something too illiquid.

Box 5: Market cap, just shows the market cap of the stock to know what size the company is.

Box 6: Number of shares, this is an additional quality of life aspect. If using low of day stops, this part calculates based on the users' inputted portfolio size and portfolio risk preference and then calculates how many stocks to buy to stay within the risk parameters. It is obviously not a sole decision making parameter nor does it guarantee any execution, but if a stock is showing an entry you want to take you can use the number of shares to help you know how many to buy. The preset is a portfolio of 10000 and a risk of 0.25%. This means that the number of shares to buy will be at the current price with lod stop that would result in a 0.25% portfolio loss. OF COURSE the actual loss depends on the execution and if the user places a stop loss order.

Hope you find it useful and feel free to give feedback! Cheers!

Position Sizing Calculator (Real-Time)█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the 5-minute timeframe, this script provides traders with continuously updated, dynamic position sizes. It enables traders to instantly determine the exact number of shares and dollar amount to use for entering a trade within their acceptable risk tolerance whenever a trade opportunity arises.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

SMB MagicSMB Magic

Overview: SMB Magic is a powerful technical strategy designed to capture breakout opportunities based on price movements, volume spikes, and trend-following logic. This strategy works exclusively on the XAU/USD symbol and is optimized for the 15-minute time frame. By incorporating multiple factors, this strategy identifies high-probability trades with a focus on risk management.

Key Features:

Breakout Confirmation:

This strategy looks for price breakouts above the previous high or below the previous low, with a significant volume increase. A breakout is considered valid when it is supported by strong volume, confirming the strength of the price move.

Price Movement Filter:

The strategy ensures that only significant price movements are considered for trades, helping to avoid low-volatility noise. This filter targets larger price swings to maximize potential profits.

Exponential Moving Average (EMA):

A long-term trend filter is applied to ensure that buy trades occur only when the price is above the moving average, and sell trades only when the price is below it.

Fibonacci Levels:

Custom Fibonacci retracement levels are drawn based on recent price action. These levels act as dynamic support and resistance zones and help determine the exit points for trades.

Take Profit/Stop Loss:

The strategy incorporates predefined take profit and stop loss levels, designed to manage risk effectively. These levels are automatically applied to trades and are adjusted based on the market's volatility.

Volume Confirmation:

A volume multiplier confirms the strength of the breakout. A trade is only considered when the volume exceeds a certain threshold, ensuring that the breakout is supported by sufficient market participation.

How It Works:

Entry Signals:

Buy Signal: A breakout above the previous high, accompanied by significant volume and price movement, occurs when the price is above the trend-following filter (e.g., EMA).

Sell Signal: A breakout below the previous low, accompanied by significant volume and price movement, occurs when the price is below the trend-following filter.

Exit Strategy:

Each position (long or short) has predefined take-profit and stop-loss levels, which are designed to protect capital and lock in profits at key points in the market.

Fibonacci Levels:

Fibonacci levels are drawn to identify potential areas of support or resistance, which can be used to guide exits and stop-loss placements.

Important Notes:

Timeframe Restriction: This strategy is designed specifically for the 15-minute time frame.

Symbol Restriction: The strategy works exclusively on the XAU/USD (Gold) symbol and is not recommended for use with other instruments.

Best Performance in Trending Markets: It works best in trending conditions where breakouts occur frequently.

Disclaimer:

Risk Warning: Trading involves risk, and past performance is not indicative of future results. Always conduct your own research and make informed decisions before trading.

ATT Model with Buy/Sell SignalsIndicator Summary

This indicator is based on the ATT (Arithmetic Time Theory) model, using specific turning points derived from the ATT sequence (3, 11, 17, 29, 41, 47, 53, 59) to identify potential market reversals. It also integrates the RSI (Relative Strength Index) to confirm overbought and oversold conditions, triggering buy and sell signals when conditions align with the ATT sequence and RSI level.

Turning Points: Detected based on the ATT sequence applied to bar count. This suggests high-probability areas where the market could turn.

RSI Filter: Adds strength to the signals by ensuring buy signals occur when RSI is oversold (<30) and sell signals when RSI is overbought (>70).

Max Signals Per Session: Limits signals to two per session to reduce over-trading.

Entry Criteria

Buy Signal: Enter a buy trade if:

The indicator displays a green "BUY" marker.

RSI is below the oversold level (default <30), suggesting a potential upward reversal.

Sell Signal: Enter a sell trade if:

The indicator displays a red "SELL" marker.

RSI is above the overbought level (default >70), indicating a potential downward reversal.

Exit Criteria

Take Profit (TP):

Define TP as a fixed percentage or point value based on the asset's volatility. For example, set TP at 1.5-2x the risk, or a predefined point target (like 50-100 points).

Alternatively, exit the position when price approaches a key support/resistance level or the next significant swing high/low.

Stop Loss (SL):

Place the SL below the recent low (for buys) or above the recent high (for sells).

Set a fixed SL in points or percentage based on the asset’s average movement range, like an ATR-based stop, or limit it to a specific risk amount per trade (1-2% of account).

Trailing into Profit

Use a trailing strategy to lock in profits and let winning trades run further. Two main options:

ATR Trailing Stop:

Set the trailing stop based on the ATR (Average True Range), adjusting every time a new candle closes. This can help in volatile markets by keeping the stop at a consistent distance based on recent price movement.

Break-Even and Partial Profits:

When the price moves in your favor by a set amount (e.g., 1:1 risk/reward), move SL to the entry (break-even).

Take partial profit at intermediate levels (e.g., 50% at 1:1 RR) and trail the remainder.

Risk Management for Prop Firm Evaluation

Prop firms often have strict rules on daily loss limits, max drawdowns, and minimum profit targets. Here’s how to align your strategy with these:

Limit Risk per Trade:

Keep risk per trade to a conservative level (e.g., 1% or lower of your account balance). This allows for more room in case of a drawdown and aligns with most prop firm requirements.

Daily Loss Limits:

Set a daily stop-loss that ensures you don’t exceed the firm’s rules. For example, if the daily limit is 5%, stop trading once you reach a 3-4% drawdown.

Avoid Over-Trading:

Stick to the max signals per session rule (one or two trades). Taking only high-probability setups reduces emotional and reactive trades, preserving capital.

Stick to a Profit Target:

Aim to meet the evaluation’s profit goal efficiently but avoid risky or oversized trades to reach it faster.

Avoid Major Economic Events:

News events can disrupt technical setups. Avoid trading around significant releases (like FOMC or NFP) to reduce the chance of sudden losses due to high volatility.

Summary

Using this strategy with discipline, a structured entry/exit approach, and tight risk management can maximize your chances of passing a prop firm evaluation. The ATT model’s turning points, combined with the RSI, provide an edge by highlighting reversal zones, while limiting trades to 1-2 per session helps maintain controlled risk.

CCI Threshold StrategyThe CCI Threshold Strategy is a trading approach that utilizes the Commodity Channel Index (CCI) as a momentum indicator to identify potential buy and sell signals in financial markets. The CCI is particularly effective in detecting overbought and oversold conditions, providing traders with insights into possible price reversals. This strategy is designed for use in various financial instruments, including stocks, commodities, and forex, and aims to capitalize on price movements driven by market sentiment.

Commodity Channel Index (CCI)

The CCI was developed by Donald Lambert in the 1980s and is primarily used to measure the deviation of a security's price from its average price over a specified period.

The formula for CCI is as follows:

CCI=(TypicalPrice−SMA)×0.015MeanDeviation

CCI=MeanDeviation(TypicalPrice−SMA)×0.015

where:

Typical Price = (High + Low + Close) / 3

SMA = Simple Moving Average of the Typical Price

Mean Deviation = Average of the absolute deviations from the SMA

The CCI oscillates around a zero line, with values above +100 indicating overbought conditions and values below -100 indicating oversold conditions (Lambert, 1980).

Strategy Logic

The CCI Threshold Strategy operates on the following principles:

Input Parameters:

Lookback Period: The number of periods used to calculate the CCI. A common choice is 9, as it balances responsiveness and noise.

Buy Threshold: Typically set at -90, indicating a potential oversold condition where a price reversal is likely.

Stop Loss and Take Profit: The strategy allows for risk management through customizable stop loss and take profit points.

Entry Conditions:

A long position is initiated when the CCI falls below the buy threshold of -90, indicating potential oversold levels. This condition suggests that the asset may be undervalued and due for a price increase.

Exit Conditions:

The long position is closed when the closing price exceeds the highest price of the previous day, indicating a bullish reversal. Additionally, if the stop loss or take profit thresholds are hit, the position will be exited accordingly.

Risk Management:

The strategy incorporates optional stop loss and take profit mechanisms, which can be toggled on or off based on trader preference. This allows for flexibility in risk management, aligning with individual risk tolerances and trading styles.

Benefits of the CCI Threshold Strategy

Flexibility: The CCI Threshold Strategy can be applied across different asset classes, making it versatile for various market conditions.

Objective Signals: The use of quantitative thresholds for entry and exit reduces emotional bias in trading decisions (Tversky & Kahneman, 1974).

Enhanced Risk Management: By allowing traders to set stop loss and take profit levels, the strategy aids in preserving capital and managing risk effectively.

Limitations

Market Noise: The CCI can produce false signals, especially in highly volatile markets, leading to potential losses (Bollinger, 2001).

Lagging Indicator: As a lagging indicator, the CCI may not always capture rapid market movements, resulting in missed opportunities (Pring, 2002).

Conclusion

The CCI Threshold Strategy offers a systematic approach to trading based on well-established momentum principles. By focusing on overbought and oversold conditions, traders can make informed decisions while managing risk effectively. As with any trading strategy, it is crucial to backtest the approach and adapt it to individual trading styles and market conditions.

References

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Lambert, D. (1980). Commodity Channel Index. Technical Analysis of Stocks & Commodities, 2, 3-5.

Pring, M. J. (2002). Technical Analysis Explained. New York: McGraw-Hill.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124-1131.

Dynamic Trading Strategy with Key Levels, Entry/Exit ManagementThis indicator provides a complete rule-based trading system, combining key levels, entry conditions, stop loss (SL), and take profit (TP) management. It’s designed to dynamically adapt to market conditions by identifying crucial support and resistance zones, determining entry points based on price action and volume, and calculating risk-based exit targets.

Key Features

Key Level Identification:

The indicator automatically identifies support and resistance levels based on recent price highs and lows within a customizable lookback period.

It adds a dynamic buffer around these levels using the Average True Range (ATR) to account for market volatility, ensuring the zones adjust to changing conditions.

Entry Conditions:

Bullish Entry: Triggers near the support zone when there’s upward price action, confirmed by volume spikes and bullish candlestick patterns (e.g., hammers, engulfing candles).

Bearish Entry: Triggers near the resistance zone when signs of rejection appear, confirmed by volume spikes and bearish candlestick patterns (e.g., shooting stars, bearish engulfing).

Entry zones are highlighted visually on the chart using green (bullish) and red (bearish) shaded boxes.

Stop Loss (SL) and Take Profit (TP):

Stop Loss: Calculated based on ATR multipliers, allowing you to set a volatility-adjusted risk level beyond the entry range.

Take Profit: Includes two profit-taking levels (TP1 and TP2), allowing for partial position exits. TP levels are calculated based on a reward-to-risk ratio, ensuring consistent profitability targets.

SL and TP levels are clearly marked with horizontal lines and labeled as SL, TP1, and TP2, helping you manage trade exits effectively.

Market Context Adaptability:

The indicator adapts to both trending and ranging market conditions. In trending markets, it favors trades that follow the trend, while in ranging markets, it focuses on reversals within the range boundaries.

Visual Aids:

Entry zones are highlighted with shaded boxes to indicate potential buy/sell regions.

SL, TP1, and TP2 levels are clearly drawn with labels, allowing for easy identification of exit points.

How to Use

Identify Key Levels: Look for support and resistance zones highlighted by the indicator on your chart.

Wait for Entry Conditions: When the price enters the entry range (marked by green or red boxes), wait for confirmation signals—such as volume spikes and candlestick patterns.

Manage Exits: Use the SL, TP1, and TP2 levels for structured trade management. Consider scaling out partially at TP1 and exiting fully at TP2.

Ideal For:

This indicator is suitable for traders who prefer a systematic approach to trading, with clear entry and exit rules. It is particularly helpful for those looking to balance risk and reward with well-defined take profit and stop loss levels.

Stoch RSI and RSI Buy/Sell Signals with MACD Trend FilterDescription of the Indicator

This Pine Script is designed to provide traders with buy and sell signals based on the combination of Stochastic RSI, RSI, and MACD indicators, enhanced by the confirmation of candle colors. The primary goal is to facilitate informed trading decisions in various market conditions by utilizing different indicators and their interactions. The script allows customization of various parameters, providing flexibility for traders to adapt it to their specific trading styles.

Usefulness

This indicator is not just a mashup of existing indicators; it integrates the functionality of multiple momentum and trend-detection methods into a cohesive trading tool. The combination of Stochastic RSI, RSI, and MACD offers a well-rounded approach to analyzing market conditions, allowing traders to identify entry and exit points effectively. The inclusion of color-coded signals (strong vs. weak) further enhances its utility by providing visual cues about the strength of the signals.

How to Use This Indicator

Input Settings: Adjust the parameters for the Stochastic RSI, RSI, and MACD to fit your trading style. Set the overbought/oversold levels according to your risk tolerance.

Signal Colors:

Strong Buy Signal: Indicated by a green label and confirmed by a green candle (close > open).

Weak Buy Signal: Indicated by a blue label and confirmed by a green candle (close > open).

Strong Sell Signal: Indicated by a red label and confirmed by a red candle (close < open).

Weak Sell Signal: Indicated by an orange label and confirmed by a red candle (close < open).

Example Trading Strategy Using This Indicator

To effectively use this indicator as part of your trading strategy, follow these detailed steps:

Setup:

Timeframe : Select a timeframe that aligns with your trading style (e.g., 15-minute for intraday, 1-hour for swing trading, or daily for longer-term positions).

Indicator Settings : Customize the Stochastic RSI, RSI, and MACD parameters to suit your trading approach. Adjust overbought/oversold levels to match your risk tolerance.

Strategy:

1. Strong Buy Entry Criteria :

Wait for a strong buy signal (green label) when the RSI is at or below the oversold level (e.g., ≤ 35), indicating a deeply oversold market. Confirm that the MACD shows a decreasing trend (bearish momentum weakening) to validate a potential reversal. Ensure the current candle is green (close > open) if candle color confirmation is enabled.

Example Use : On a 1-hour chart, if the RSI drops below 35, MACD shows three consecutive bars of decreasing negative momentum, and a green candle forms, enter a buy position. This setup signals a robust entry with strong momentum backing it.

2. Weak Buy Entry Criteria :

Monitor for weak buy signals (blue label) when RSI is above the oversold level but still below the neutral (e.g., between 36 and 50). This indicates a market recovering from an oversold state but not fully reversing yet. These signals can be used for early entries with additional confirmations, such as support levels or higher timeframe trends.

Example Use : On the same 1-hour chart, if RSI is at 45, the MACD shows momentum stabilizing (not necessarily negative), and a green candle appears, consider a partial or cautious entry. Use this as an early warning for a potential bullish move, especially when higher timeframe indicators align.

3. Strong Sell Entry Criteria :

Look for a strong sell signal (red label) when RSI is at or above the overbought level (e.g., ≥ 65), signaling a strong overbought condition. The MACD should show three consecutive bars of increasing positive momentum to indicate that the bullish trend is weakening. Ensure the current candle is red (close < open) if candle color confirmation is enabled.

Example Use : If RSI reaches 70, MACD shows increasing momentum that starts to level off, and a red candle forms on a 1-hour chart, initiate a short position with a stop loss set above recent resistance. This is a high-confidence signal for potential price reversal or pullback.

4. Weak Sell Entry Criteria :

Use weak sell signals (orange label) when RSI is between the neutral and overbought levels (e.g., between 50 and 64). These can indicate potential short opportunities that might not yet be fully mature but are worth monitoring. Look for other confirmations like resistance levels or trendline touches to strengthen the signal.

Example Use : If RSI reads 60 on a 1-hour chart, and the MACD shows slight positive momentum with signs of slowing down, place a cautious sell position or scale out of existing long positions. This setup allows you to prepare for a possible downtrend.

Trade Management:

Stop Loss : For buy trades, place stop losses below recent swing lows. For sell trades, set stops above recent swing highs to manage risk effectively.

Take Profit : Target nearby resistance or support levels, apply risk-to-reward ratios (e.g., 1:2), or use trailing stops to lock in profits as price moves in your favor.

Confirmation : Align these signals with broader trends on higher timeframes. For example, if you receive a weak buy signal on a 15-minute chart, check the 1-hour or daily chart to ensure the overall trend is not bearish.

Real-World Example: Imagine trading on a 15-minute chart :

For a buy:

A strong buy signal (green) appears when the RSI dips to 32, MACD shows declining bearish momentum, and a green candle forms. Enter a buy position with a stop loss below the most recent support level.

Alternatively, a weak buy signal (blue) appears when RSI is at 47. Use this as a signal to start monitoring the market closely or enter a smaller position if other indicators (like support and volume analysis) align.

For a sell:

A strong sell signal (red) with RSI at 72 and a red candle signals to short with conviction. Place your stop loss just above the last peak.

A weak sell signal (orange) with RSI at 62 might prompt caution but can still be acted on if confirmed by declining volume or touching a resistance level.

These strategies show how to blend both strong and weak signals into your trading for more nuanced decision-making.

Technical Analysis of the Code

1. Stochastic RSI Calculation:

The script calculates the Stochastic RSI (stochRsiK) using the RSI as input and smooths it with a moving average (stochRsiD).

Code Explanation : ta.stoch(rsi, rsi, rsi, stochLength) computes the Stochastic RSI, and ta.sma(stochRsiK, stochSmoothing) applies smoothing.

2. RSI Calculation :

The RSI is computed over a user-defined period and checks for overbought or oversold conditions.

Code Explanation : rsi = ta.rsi(close, rsiLength) calculates RSI values.

3. MACD Trend Filter :

MACD is calculated with fast, slow, and signal lengths, identifying trends via three consecutive bars moving in the same direction.

Code Explanation : = ta.macd(close, macdLengthFast, macdLengthSlow, macdSignalLength) sets MACD values. Conditions like macdLine < macdLine confirm trends.

4. Buy and Sell Conditions :

The script checks Stochastic RSI, RSI, and MACD values to set buy/sell flags. Candle color filters further confirm valid entries.

Code Explanation : buyConditionMet and sellConditionMet logically check all conditions and toggles (enableStochCondition, enableRSICondition, etc.).

5. Signal Flags and Confirmation :

Flags track when conditions are met and ensure signals only appear on appropriate candle colors.

Code Explanation : Conditional blocks (if statements) update buyFlag and sellFlag.

6. Labels and Alerts :

The indicator plots "BUY" or "SELL" labels with the RSI value when signals trigger and sets alerts through alertcondition().

Code Explanation : label.new() displays the signal, color-coded for strength based on RSI.

NOTE : All strategies can be enabled or disabled in the settings, allowing traders to customize the indicator to their preferences and trading styles.

Trade Manager 2Hi Traders,

this manager will make it easier for you to enter lots into your trading platform. Just go to the indicator settings, set your trading account amount, RRR, % risk and then give ok. If you then know where you want to put the stop loss then reopen, enter the value and hit ok again. The chart will show you exactly the stop loss and take profit as you wanted. The stop loss will always stay where you enter it and the take profit will move with the lot size as the price goes further or closer to the stop loss.

This should help when entering the number of lots, TP, SL into the platform.

The Exact IndicatorStruggling to get in on a trade? Don't know where to take profits? This indicator might help - it only displays the Buy, Stop Loss and Take profit points when certain conditions are met.

The indicator combines a moving average crossover strategy with trend analysis to identify potential buy opportunities in the market. It utilises a short-term and long-term Simple Moving Average (SMA) to generate buy signals when the short-term SMA crosses above the long-term SMA. Additionally, it displays take profit and stop loss levels, along with a background colour indicating the overall trend strength.

Pros :

Clear Signals : Provides straightforward buy signals based on a well-known crossover strategy, making it easy for traders to identify entry points.

Visual Aids : The inclusion of take profit and stop loss levels, along with background trend colors, enhances decision-making and risk management.

Trend Awareness : The background colour changes based on trend strength, allowing traders to quickly assess market conditions.

Cons :

Lagging Indicator : Moving averages are inherently lagging, which can result in delayed signals, especially in volatile markets.

False Signals : Crossover strategies can produce false signals during sideways or choppy market conditions, leading to potential losses.

Limited Scope : The indicator focuses primarily on buy signals, potentially missing out on other trading opportunities (like short-selling) in a bearish market.

Overall, while this indicator can be a useful tool for identifying bullish trends and potential entry points, traders should use it in conjunction with other analysis methods and risk management strategies to mitigate its limitations.

E9 Shark-32 Pattern Strategy The E9 Shark-32 Pattern is a powerful trading tool designed to capitalize on the Shark-32 pattern—a specific Candlestick pattern.

The Shark-32 Pattern: What Is It?

The Shark-32 pattern is a technical formation that occurs when the following conditions are met:

Higher Highs and Lower Lows: The low of two bars ago is lower than the previous bar, and the previous bar's low is lower than the current bar. At the same time, the high of two bars ago is higher than the previous bar, and the previous bar’s high is higher than the current bar.

This unique setup forms the "Shark-32" pattern, which signals potential volume squeezes and trend changes in the market.

How Does the Strategy Work?

The E9 Shark-32 Pattern Strategy builds upon this pattern by defining clear entry and exit rules based on the pattern's confirmation. Here's a breakdown of how the strategy operates:

1. Identifying the Shark-32 Pattern

When the Shark-32 pattern is confirmed, the strategy "locks" the high and low prices from the initial bar of the pattern. These locked prices serve as key levels for future trade entries and exits.

2. Entry Conditions

The strategy waits for the price to cross the pattern's locked high or low, signaling potential market direction.

Long Entry: A long trade is triggered when the closing price crosses above the locked pattern high (green line).

Short Entry: A short trade is triggered when the closing price crosses below the locked pattern low (red line).

The strategy ensures that only one trade is taken for each Shark-32 pattern, preventing overtrading and allowing traders to focus on high-probability setups.

3. Stop Loss and Take Profit Levels

The strategy has built-in risk management through stop-loss and take-profit levels, which are visually represented by the lines on the chart:

Stop Loss:

Stop loss can be adjusted in settings.

Take Profit:

For long trades: The take-profit target is set at the upper white dotted line, which is projected above the pattern high.

For short trades: The take-profit target is set at the lower white dotted line, which is projected below the pattern low.

These clearly defined levels help traders to manage risk effectively while maximizing potential returns.

4. Visual Cues

To make trading decisions even easier, the strategy provides helpful visual cues:

Green Line (Pattern High): This line represents the high of the Shark-32 pattern and serves as a resistance level and short entry signal.

Red Line (Pattern Low): This line represents the low of the Shark-32 pattern and serves as a support level and long entry signal.

White Dotted Lines: These lines represent potential profit targets, projected both above and below the pattern. They help traders define where the market might go next.

Additionally, the strategy highlights the pattern formation with color-coded bars and background shading to draw attention to the Shark-32 pattern when it is confirmed. This adds a layer of visual confirmation, making it easier to spot opportunities in real-time.

5. No Repeated Trades

An important aspect of the strategy is that once a trade is taken (either long or short), no additional trades are executed until a new Shark-32 pattern is identified. This ensures that only valid and confirmed setups are acted upon.

ATR+StdTR Band and Trailing StopThis Pine Script code plots the "ATR+StdTR Band and Trailing Stop," serving as a tool for volatility-based risk management and trend detection. While bands are typically set using a multiple of ATR, this script uses StdTR (the True Range standard deviation) and sets the band width based on ±(ATR + n times StdTR). StdTR is a great tool for detecting price volatility and anomalies, allowing traders to adapt to rapid changes in extreme market conditions. This helps traders proactively manage risk during sudden market fluctuations.

The following features are provided:

Table Display

A table is shown on the chart, allowing traders to visually track the current ATR value, StdTR (σ), and the long/short stop-loss levels (±ATR ± nσ). This enables real-time monitoring of risk management data.

Band Plots

The script plots bands that combine ATR with StdTR (nσ).

The upper and lower bands are calculated using the previous candle’s closing price (the source is customizable) and are plotted as ±(ATR + nσ), providing a clear visual of the price range.

ATR ± nσ Trailing Stop

The trailing stop dynamically adjusts the stop-loss levels based on price movements. In an uptrend, the stop-loss rises, while in a downtrend, it lowers, helping traders lock in profits while minimizing losses during significant reversals.

Breakout Detection

Breakouts are detected when the price exceeds the upper band or drops below the lower band. A visual marker (X) is displayed on the chart, allowing traders to quickly recognize when the price has moved beyond normal volatility ranges, making it easier to respond to trend formations or reversals.

Customization Points:

The ATR period and StdTR (n) are fully customizable.

The source for ATR band calculation can be adjusted, allowing traders to choose from close, open, high, low, etc.

The table’s display position and design (text color, size, etc.) can be customized to present the information clearly and effectively.

Options Series - P_SAR And Supertrend

The provided PineScript combines two well-known indicators—Parabolic SAR (P_SAR) and Supertrend—to create a comprehensive trading tool. Here are some powerful insights and the importance of this script:

⭐ 1. Supertrend Indicator:

What it does: The Supertrend indicator is based on the Average True Range (ATR) and is used to identify trend direction. When the price is above the Supertrend line, it suggests an uptrend, and when below, a downtrend.

Insights:

Trend Following: By adjusting the ATR length (atrPeriod) and the multiplier (factor), you can fine-tune the sensitivity of the Supertrend. A smaller ATR or factor results in more frequent trend changes, whereas larger values make the indicator more robust but slower to react.

Trend Visualization: The script highlights trends with the help of green and red lines, offering a clear visual cue for traders. The uptrend is filled with a translucent green and the downtrend with red, allowing quick identification of market momentum.

⭐ 2. Parabolic SAR (P_SAR):

What it does: The Parabolic SAR is a time/price-based indicator that helps identify potential reversals in the market. The dots (SAR) follow the price and move closer to it as the trend progresses.

Insights:

Trailing Stops: This is commonly used by traders to trail stop losses, as the SAR moves closer to price as the trend strengthens.

Combining with Supertrend: The SAR dots in this script act as an additional confirmation for trend direction. For instance, when the price is above both the SAR and Supertrend, it strongly suggests an uptrend.

⭐ 3. Bar Coloring Based on Trend Confirmation:

What it does: The script calculates conditions based on whether the price is above or below both the Supertrend and SAR values.

Insights:

Bullish/Bearish Confirmation: The combination of these two indicators provides a stronger confirmation of trend direction compared to using either one alone. For example:

Green Bars: If the price is above both the Supertrend and SAR, it signals a strong uptrend (bullish).

Red Bars: If the price is below both, it suggests a strong downtrend (bearish).

Visual Alerts: The candle colors are adjusted based on these conditions, providing a quick visual alert for traders to take action.

⭐ 4. Importance of Using Both Supertrend and P_SAR:

Multiple Confirmations: Combining the Supertrend and Parabolic SAR increases the accuracy of trend-following strategies. Each indicator has its strengths: Supertrend is good for identifying the overall trend, while the SAR excels at identifying potential reversals.

Risk Management: This script can help you not only identify trends but also manage your positions more effectively. The Parabolic SAR, for example, can serve as a dynamic stop-loss level, while the Supertrend can help you stay in trades longer by smoothing out noise in the market.

⭐ 5. Customizable Inputs:

Adaptability: The user can adjust the ATR period, factor, start, increment, and maximum values, tailoring the script to different market conditions and timeframes. This flexibility is essential, as each asset class or market may require different parameter settings.

⭐ 6. Practical Application in Trading:

Entry and Exit Signals: The script can be used to generate entry and exit signals. For instance:

Buy Signal: When the bar turns green (price is above Supertrend and SAR), it could be a signal to go long.

Sell Signal: When the bar turns red (price is below Supertrend and SAR), it could be a signal to go short or exit a long position.

Stop-Loss Placement: The Parabolic SAR dots can act as trailing stop-loss levels, helping traders lock in profits as trends progress.

Trend Continuation vs. Reversal: The Supertrend provides a broader view of the trend, while the Parabolic SAR provides pinpoint entry/exit signals for reversals.

🚀 Conclusion:

This script is a robust combination of trend-following and reversal indicators, making it a versatile tool for traders. The dual confirmation from Supertrend and Parabolic SAR reduces false signals, and the color-coded bars provide quick insights into market conditions. When used properly, this can greatly improve your ability to catch trends early, exit at the right moment, and manage risk effectively.

Descriptive Backtesting Framework (DBF)As the name suggests, this is a backtesting framework made to offer full backtesting functionality to any custom indicator in a visually descriptive way.

Any trade taken will be very clear to visualize on the chart and the equity line will be updated live allowing us to use the REPLAY feature to view the strategy performing in real time.

Stops and Targets will also get draw on the chart with labels and tooltips and there will be a table on the top right corner displaying lots of descriptive metrics to measure your strategy's performance.

IF YOU DECIDE TO USE THIS FRAMEWORK, PLEASE READ **EVERYTHING** BELOW

HOW TO USE IT

Step 1 - Insert Your Strategy Indicators:

Inside this framework's code, right at the beginning, you will find a dedicated section where you can manually insert any set of indicators you desire.

Just replace the example code in there with your own strategy indicators.

Step 2 - Specify The Conditions To Take Trades:

After that, there will be another section where you need to specify your strategy's conditions to enter and exit trades.

When met, those conditions will fire the trading signals to the trading engine inside the framework.

If you don't wish to use some of the available signals, please just assign false to the signal.

DO NOT DELETE THE SIGNAL VARIABLES

Step 3 - Specify Entry/Exit Prices, Stops & Targets:

Finally you'll reach the last section where you'll be able to specify entry/exit prices as well as add stops and targets.

On most cases, it's easier and more reliable to just use the close price to enter and exit trades.

If you decide to use the open price instead, please remember to change step 2 so that trades are taken on the open price of the next candle and not the present one to avoid the look ahead bias.

Stops and targets can be set in any way you want.

Also, please don't forget to update the spread. If your broker uses commissions instead of spreads or a combination of both, you'll need to manually incorporate those costs in this step.

And that's it! That's all you have to do.

Below this section you'll now see a sign warning you about not making any changes to the code below.

From here on, the framework will take care of executing the trades and calculating the performance metrics for you and making sure all calculations are consistent.

VISUAL FEATURES:

Price candles get painted according to the current trade.

They will be blue during long trades, purple on shorts and white when no trade is on.

When the framework receives the signals to start or close a trade, it will display those signals as shapes on the upper and lower limits of the chart:

DIAMOND: represents a signal to open a trade, the trade direction is represented by the shape's color;

CROSS: means a stop loss was triggered;

FLAG: means a take profit was triggered;

CIRCLE: means an exit trade signal was fired;

Hovering the mouse over the trade labels will reveal:

Asset Quantity;

Entry/Exit Prices;

Stops & Targets;

Trade Profit;

Profit As Percentage Of Trade Volume;

**Please note that there's a limit as to how many labels can be drawn on the chart at once.**

If you which to see labels from the beginning of the chart, you'll probably need to use the replay feature.

PERFORMANCE TABLE:

The performance table displays several performance metrics to evaluate the strategy.

All the performance metrics here are calculated by the framework. It does not uses the oficial pine script strategy tester.

All metrics are calculated in real time. If using the replay feature, they will be updated up to the last played bar.

Here are the available metrics and their definition:

INITIAL EQUITY: the initial amount of money we had when the strategy started, obviously...;

CURRENT EQUITY: the amount of money we have now. If using the replay feature, it will show the current equity up to the last bar played. The number on it's right side shows how many times our equity has been multiplied from it's initial value;

TRADE COUNT: how many trades were taken;

WIN COUNT: how many of those trades were wins. The percentage at the right side is the strategy WIN RATE;

AVG GAIN PER TRADE: the average percentage gain per trade. Very small values can indicate a fragile strategy that can behave in unexpected ways under high volatility conditions;

AVG GAIN PER WIN: the average percentage gain of trades that were profitable;

AVG GAIN PER LOSS: the average percentage loss on trades that were not profitable;

EQUITY MAX DD: the maximum drawdown experienced by our equity during the entire strategy backtest;

TRADE MAX DD: the maximum drawdown experienced by our equity after one single trade;

AVG MONTHLY RETURN: the compound monthly return that our strategy was able to create during the backtested period;

AVG ANNUAL RETURN: this is the strategy's CAGR (compound annual growth rate);

ELAPSED MONTHS: number of months since the backtest started;

RISK/REWARD RATIO: shows how profitable the strategy is for the amount of risk it takes. Values above 1 are very good (and rare). This is calculated as follows: (Avg Annual Return) / mod(Equity Max DD). Where mod() is the same as math.abs();

AVAILABLE SETTINGS:

SPREAD: specify your broker's asset spread

ENABLE LONGS / SHORTS: you can keep both enable or chose to take trades in only one direction

MINIMUM BARS CLOSED: to avoid trading before indicators such as a slow moving average have had time to populate, you can manually set the number of bars to wait before allowing trades.

INITIAL EQUITY: you can specify your starting equity

EXPOSURE: is the percentage of equity you wish to risk per trade. When using stops, the strategy will automatically calculate your position size to match the exposure with the stop distance. If you are not using stops then your trade volume will be the percentage of equity specified here. 100 means you'll enter trades with all your equity and 200 means you'll use a 2x leverage.

MAX LEVERAGE ALLOWED: In some situations a short stop distance can create huge levels of leverage. If you want to limit leverage to a maximum value you can set it here.

SEVERAL PLOTTING OPTIONS: You'll be able to specify which of the framework visuals you wish to see drawn on the chart.

FRAMEWORK **LIMITATIONS**:

When stop and target are both triggered in the same candle, this framework isn't able to enter faster timeframes to check which one was triggered first, so it will take the pessimistic assumption and annul the take profit signal;

This framework doesn't support pyramiding;

This framework doesn't support both long and short positions to be active at the same time. So for example, if a short signal is received while a long trade is open, the framework will close the long trade and then open a short trade;

FINAL CONSIDERATIONS:

I've been using this framework for a good time and I find it's better to use and easier to analyze a strategy's performance then relying on the oficial pine script strategy tester. However, I CANNOT GUARANTEE IT TO BE BUG FREE.

**PLEASE PERFORM A MANUAL BACKTEST BEFORE USING ANY STRATEGY WITH REAL MONEY**

Lot Size Calculator by MenolakRugiThe Lot Size Formula in forex trading is a critical tool that offers several key benefits to traders:

🟢Risk Management: By using the formula, traders can control the amount of capital they risk on each trade. This helps prevent excessive losses by aligning the lot size with a predefined risk tolerance, such as 1% or 2% of the account balance.

🟢Consistent Position Sizing: The formula ensures that position sizes are calculated based on the specific trade setup, including the distance to the stop loss. This consistency helps avoid over-leveraging and reduces the emotional aspect of trading.

🟢Adaptability: The lot size can be adjusted according to different currency pairs and market conditions. This flexibility ensures that traders can apply the formula across various trading instruments and environments.

🟢Improved Profit Potential: By managing risk effectively, traders can protect their capital while maximizing profit opportunities. When losses are controlled, traders are able to stay in the market longer and compound their gains over time.

🟢Precision in Trade Planning: Calculating the lot size allows traders to plan their trades more precisely, aligning their strategies with the amount they are willing to risk. This leads to more disciplined and structured trading, reducing impulsive decisions.

In summary, the lot size formula helps maintain a balanced approach to trading, where both risk and reward are carefully managed to increase the chances of long-term success.

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

False Breakouts [TradingFinder] Fake Breakouts Failure🔵 Introduction

Technical indicators are essential tools for analysts and traders in financial markets, helping them predict price movements and make better trading decisions. One of the key concepts in technical analysis that should be carefully considered is the "False Breakout."

This phenomenon occurs when a price temporarily breaks through a significant support or resistance level but fails to hold and quickly returns to its previous range. Understanding this concept and applying it in trading can reduce risks and increase profitability.

🟣 What is a False Breakout?

A Fake Breakout, as the name suggests, refers to a breakout that appears to occur but fails to sustain, leading the price to quickly revert back to its previous range. This situation often happens when inexperienced or non-professional traders, under psychological pressure and eager to enter the market quickly, initiate trades.

This creates opportunities for professional traders to take advantage of these short-term fluctuations and execute successful trades.

🟣 The Importance of Recognizing False Breakouts

Recognizing False Breakouts is crucial for any trader aiming for success in financial markets. False Breakouts typically occur when the market approaches a critical support or resistance level.

In these situations, many traders are waiting to see if the price will break through this level. However, when the price quickly returns to its previous range, it indicates weakness in the movement and the inability to sustain the breakout.

🟣 How to identify False Breakouts?

To identify Fake Breakouts, it is important to carefully analyze price charts and look for signs of a quick price reversal after breaking a key level.

Here are some chart patterns that may help you identify a False Breakout :

1. Pin Bar Pattern : The Pin Bar is a candlestick pattern that indicates a price reversal. This pattern usually appears near support and resistance levels, showing that the price attempted to break through a key level but failed and reversed.

2. Fakey Pattern : This pattern, which consists of several candlesticks, indicates a False Breakout and a quick price return to the previous range. It usually appears near key levels and can signal a trend reversal.

3. Using Multiple Timeframes : One way to identify False Breakouts is by using charts of different timeframes. Sometimes, a breakout on a one-hour chart may be a False Breakout on a daily chart. Analyzing charts across multiple timeframes can help you accurately identify this phenomenon.

🔵 How to Use

Once you identify a False Breakout, you can use it as a trading signal. For this, it is best to look for trading opportunities in the opposite direction of the False Breakout. In other words, if a False Breakout occurs at a resistance level, you might consider selling opportunities, and if it happens at a support level, you might look for buying opportunities.

Here are some key points for trading based on False Breakouts :

1. Patience and Discipline : Patience and discipline are crucial when trading with False Breakouts. Wait for the False Breakout to clearly form before entering a trade.

2. Use Stop Loss : Setting an appropriate stop loss is vital when trading based on False Breakouts. Typically, the stop loss can be placed near the level where the False Breakout occurred.

3. Seek Confirmations : Before entering a trade, look for additional confirmations. These can include other analyses or technical indicators that show the price is likely to return to its previous level.

🔵 Settings

🟣 Logical settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Bac k: You can set the number of swings that will go back for checking.

🟣 Display settings

Displaying or not displaying swings and setting the color of labels and lines.

🟣 Alert Settings

Alert False Breakout : Enables alerts for Breakout.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

🔵Conclusion

False Breakouts, as a key concept in technical analysis, are powerful tools for identifying sudden price changes and using them in trading. Understanding this phenomenon and applying it can help traders perform better in financial markets and avoid potential losses.

To benefit from False Breakouts, traders need to carefully analyze charts and use the appropriate analytical tools. By leveraging this strategy, traders can achieve lower-risk and higher-reward trades.

Multi-Factor StrategyThis trading strategy combines multiple technical indicators to create a systematic approach for entering and exiting trades. The goal is to capture trends by aligning several key indicators to confirm the direction and strength of a potential trade. Below is a detailed description of how the strategy works:

Indicators Used

MACD (Moving Average Convergence Divergence):

MACD Line: The difference between the 12-period and 26-period Exponential Moving Averages (EMAs).

Signal Line: A 9-period EMA of the MACD line.